Compliance Just Got Easier: Stay ahead of regulatory changes with instant notifications on updates that matter.

['Air Programs']

['Mobile Emission Sources']

12/09/2024

Copyright 2026 J. J. Keller & Associate, Inc. For re-use options please contact copyright@jjkeller.com or call 800-558-5011.

ENVIRONMENTAL PROTECTION AGENCY

[EPA-HQ-OAR-2021-0208; FRL 8469-01-OAR]

RIN 2060-AV13

Revised 2023 and Later Model Year Light-Duty Vehicle Greenhouse Gas Emissions Standards

AGENCY: Environmental Protection Agency (EPA).

ACTION: Final rule.

SUMMARY: The Environmental Protection Agency (EPA) is revising the greenhouse gas (GHG) emissions standards under the Clean Air Act section 202(a) for light-duty vehicles for 2023 and later model years to make the standards more stringent. On January 20, 2021, President Biden issued Executive Order 13990 “Protecting Public Health and the Environment and Restoring Science To Tackle the Climate Crisis” directing EPA to consider whether to propose suspending, revising, or rescinding the standards previously revised under the “The Safer Affordable Fuel-Efficient (SAFE) Vehicles Rule for Model Years 2021-2026 Passenger Cars and Light Trucks,” promulgated in April 2020. EPA is revising the GHG standards to be more stringent than the SAFE rule standards in each model year from 2023 through 2026. EPA is also including temporary targeted flexibilities to address the lead time of the final standards and to incentivize the production of vehicles with zero and near-zero emissions technology. In addition, EPA is making technical amendments to clarify and streamline our regulations.

DATES: This final rule is effective on February 28, 2022. The incorporation by reference of certain publications listed in this regulation is approved by the Director of the Federal Register as of February 28, 2022.

ADDRESSES: EPA has established a docket for this action under Docket ID No. EPA-HQ-OAR-2021-0208. All documents in the docket are listed on the http://www.regulations.gov website. Although listed in the index, some information is not publicly available, e.g., CBI or other information whose disclosure is restricted by statute. Certain other material, such as copyrighted material, is not placed on the internet and will be publicly available only in hard copy form. Publicly available docket materials are available electronically through http://www.regulations.gov.

FOR FURTHER INFORMATION CONTACT:

Elizabeth Miller, Office of Transportation and Air Quality, Assessment and Standards Division (ASD), Environmental Protection Agency, 2000 Traverwood Drive, Ann Arbor, MI 48105; telephone number: (734) 214-4703; email address: miller.elizabeth@epa.gov.

SUPPLEMENTARY INFORMATION:

Does this action apply to me?

This action affects companies that manufacture or sell passenger automobiles (passenger cars) and non-passenger automobiles (light trucks) as defined in 49 CFR part 523. Regulated categories and entities include:

| Category | NAICS codes A | Examples of potentially regulated entities |

|---|---|---|

| A North American Industry Classification System (NAICS). | ||

| Industry | 336111, 336112 | Motor Vehicle Manufacturers. |

| Industry | 811111, 811112, 811198, 423110 | Commercial Importers of Vehicles and Vehicle Components. |

| Industry | 335312, 811198 | Alternative Fuel Vehicle Converters. |

This list is not intended to be exhaustive, but rather provides a guide regarding entities likely to be regulated by this action. To determine whether particular activities may be regulated by this action, you should carefully examine the regulations. You may direct questions regarding the applicability of this action to the person listed in FOR FURTHER INFORMATION CONTACT .

Table of Contents

I. Executive Summary

A. Purpose of This Final Rule and Legal Authority

1. Final Light-Duty GHG Standards for Model Years 2023-2026

2. Why does EPA believe the final standards are appropriate under the CAA?

B. Summary of Final Light-Duty Vehicle GHG Program

1. Final Revised GHG Emissions Standards

2. Final Compliance Flexibilities and Advanced Technology Incentives

C. Analytical Support for the Final Revised Standards

D. Summary of Costs, Benefits and GHG Emission Reductions of the Final Program

E. How has EPA considered environmental justice in this final rule?

F. Affordability and Equity

II. EPA Standards for MY 2023-2026 Light-Duty Vehicle GHGs

A. Model Year 2023-2026 GHG Standards for Light-Duty Vehicles, Light-Duty Trucks, and Medium-Duty Passenger Vehicles

1. What fleet-wide emissions levels correspond to the CO2 standards?

2. What are the final CO2 attribute-based standards?

3. EPA's Statutory Authority Under the CAA

4. Averaging, Banking, and Trading Provisions for CO2 Standards

5. Certification, Compliance, and Enforcement

6. On-Board Diagnostics Program Updates

7. Stakeholder Engagement

8. How do EPA's final standards relate to NHTSA's CAFE proposal and to California's GHG program?

B. Manufacturer Compliance Flexibilities

1. Multiplier Incentives for Advanced Technology Vehicles

2. Full-Size Pickup Truck Incentives

3. Off-Cycle Technology Credits

4. Air Conditioning System Credits

5. Natural Gas Vehicles Technical Correction

C. What alternatives did EPA analyze?

III. Technical Assessment of the Final CO2 Standards

A. What approach did EPA use in analyzing the standards?

B. Projected Compliance Costs and Technology Penetrations

1. GHG Targets and Compliance Levels

2. Projected Compliance Costs per Vehicle

3. Technology Penetration Rates

C. Are the final standards feasible?

D. How did EPA consider alternatives in selecting the final program?

IV. How does this final rule reduce GHG emissions and their associated effects?

A. Impact on GHG Emissions

B. Climate Change Impacts From GHG Emissions

C. Global Climate Impacts and Benefits Associated With the Final Rule's Estimated GHG Emissions Reductions

V. How would the final rule impact non-GHG emissions and their associated effects?

A. Impact on Non-GHG Emissions

B. Health and Environmental Effects Associated With Exposure to Non-GHG Pollutants Impacted by the Final Standards

C. Air Quality Impacts of Non-GHG Pollutants

VI. Basis for the Final GHG Standards Under CAA Section 202(a)

A. Consideration of Technological Feasibility and Lead Time

B. Consideration of Vehicle Costs of Compliance

C. Consideration of Impacts on Consumers

D. Consideration of Emissions of GHGs and Other Air Pollutants

E. Consideration of Energy, Safety and Other Factors

F. Balancing of Factors Under CAA 202(a)

VII. What are the estimated cost, economic, and other impacts of the rule?

A. Conceptual Framework for Evaluating Consumer Impacts

B. Vehicle Sales Impacts

C. Changes in Fuel Consumption

D. Greenhouse Gas Emission Reduction Benefits

E. Non-Greenhouse Gas Health Impacts

F. Energy Security Impacts

G. Impacts of Additional Driving

H. Safety Considerations in Establishing GHG Standards

I. Summary of Costs and Benefits

J. Impacts on Consumers of Vehicle Costs and Fuel Savings

K. Employment Impacts

L. Environmental Justice

1. GHG Impacts

2. Non-GHG Impacts

M. Affordability and Equity Impacts

VIII. Statutory and Executive Order Reviews

A. Executive Order 12866: “Regulatory Planning and Review and Executive Order 13563: Improving Regulation and Regulatory Review”

B. Paperwork Reduction Act

C. Regulatory Flexibility Act

D. Unfunded Mandates Reform Act

E. Executive Order 13132: “Federalism”

F. Executive Order 13175: “Consultation and Coordination With Indian Tribal Governments”

G. Executive Order 13045: “Protection of Children From Environmental Health Risks and Safety Risks”

H. Executive Order 13211: “Energy Effects”

I. National Technology Transfer and Advancement Act and 1 CFR Part 51

J. Executive Order 12898: “Federal Actions To Address Environmental Justice in Minority Populations and Low-Income Populations”

K. Congressional Review Act (CRA)

L. Judicial Review

IX. Statutory Provisions and Legal Authority

I. Executive Summary

A. Purpose of This Final Rule and Legal Authority

1. Final Light-Duty GHG Standards for Model Years 2023-2026

In this final action, the Environmental Protection Agency (EPA) is establishing revised, more stringent national greenhouse gas (GHG) emissions standards for passenger cars and light trucks under section 202(a) of the Clean Air Act (CAA), 42 U.S.C. 7521(a). Section 202(a) requires EPA to establish standards for emissions of air pollutants from new motor vehicles which, in the Administrator's judgment, cause or contribute to air pollution which may reasonably be anticipated to endanger public health or welfare.

This action finalizes the standards that EPA proposed in August 2021. 1

1 86 FR 43726.

In response to Executive Order 13990 “Protecting Public Health and the Environment and Restoring Science To Tackle the Climate Crisis,” 2 EPA conducted an extensive review of the existing regulations, which resulted in EPA proposing revised, more stringent standards. In the proposed rule, EPA sought public comment on a range of alternative standards, including alternatives that were less stringent (Alternative 1) and more stringent (Alternative 2) than the proposed standards as well as standards that were even more stringent (in the range of 5-10 grams CO2 per mile (g/mile)) for model year (MY) 2026. As discussed in Section I.A.2 of this preamble, based on public comments and EPA's final analyses, EPA is finalizing standards consistent with the standards we proposed for MYs 2023 and 2024, and more stringent than those we proposed for MYs 2025 and 2026. EPA's final standards for MYs 2025 and 2026 are the most stringent standards considered in the proposed rule and establish the most stringent GHG standards ever set for the light-duty vehicle sector. EPA is revising the light-duty vehicle GHG standards for MYs 2023 through 2026, which had been previously revised by the SAFE rule, in part by building on earlier EPA actions and supporting analyses that established or maintained stringent standards. For example, in 2012, EPA issued a final rule establishing light-duty vehicle GHG standards for MYs 2017-2025, 3 which were supported by analyses of compliance costs, lead time and other relevant factors. 4 That rule and its analyses also accounted for the development and availability of advanced GHG emission-reducing vehicle technologies, which demonstrated that the standards were appropriate under section 202(a) of the CAA.

2 86 FR 7037, January 25, 2021. “[T]he head of the relevant agency, as appropriate and consistent with applicable law, shall consider publishing for notice and comment a proposed rule suspending, revising, or rescinding the agency action[s set forth below] within the time frame specified.” “Establishing Ambitious, Job-Creating Fuel Economy Standards: . . . `The Safer Affordable Fuel-Efficient (SAFE) Vehicles Rule for Model Years 2021-2026 Passenger Cars and Light Trucks,' 85 FR 24174 (April 30, 2020), by July 2021. In considering whether to propose suspending, revising, or rescinding the latter rule, the agency should consider the views of representatives from labor unions, States, and industry.”

3 EPA's model year emission standards also apply in subsequent model years, unless revised, e.g., MY 2025 standards issued in the 2012 rule also applied to MY 2026 and beyond.

4 77 FR 62624, October 15, 2012.

This final rule is also supported by updated analyses that consider the most recent technical and scientific data and continuing developments in the automotive industry, as well as public comments on the proposed rule. As noted in the proposed rule, auto manufacturers continue to implement a broad array of advanced gasoline vehicle GHG emission-reducing technologies at a rapid pace throughout their vehicle fleets. Even more notably, vehicle electrification technologies are advancing at a historic pace as battery costs continue to decline and automakers continue to announce plans for an increasing diversity and production volume of zero- and near-zero emission vehicle models. These trends continue to support EPA's decision to revise the existing GHG standards, particularly in light of factors indicating that more stringent near-term standards are feasible at reasonable cost and would achieve significantly greater GHG emissions reductions and public health and welfare benefits than the existing program.

In developing this final rule, EPA considered comments received during the public comment period, including during the public hearing. EPA held a two-day virtual public hearing on August 25 and 26, 2021 and heard from approximately 175 speakers. During the public comment period that ended on September 27, 2021, EPA received more than 188,000 written comments. This preamble, together with the accompanying Response to Comments (RTC) document, responds to all significant comments we received on the proposed rule.

Comments from automakers that historically have produced primarily internal combustion engine (ICE) vehicles, such as comments by the Alliance for Automotive Innovation (hereafter referred to as “the Alliance”) as well as comments by several individual automakers, generally supported the proposed standards and did not support the more stringent alternatives on which we requested comment. A common theme from these commenters is that EPA should not overly rely on high penetrations of electric vehicles (EVs) during the period through MY 2026 as a means of compliance for the industry, because of uncertainty about the degree of availability of EV charging infrastructure and market uptake of EVs in this time frame. The United Auto Workers (UAW) commented similarly, generally supporting the proposed standards and flexibilities but not supporting more stringent standards or reduced flexibilities. In contrast, automakers producing (or planning to produce) only EVs (Tesla, Rivian, and Lucid) supported standards more stringent than the proposed standards, and they generally did not support the proposed flexibilities.

Comments from organizations representing environmental, public health, and consumer groups as well as comments from many states and local governments generally state that in this rulemaking EPA should address public health, climate change, and social equity in a robust manner. These commenters expressed nearly universal support for the more stringent Alternative 2; many also support an additional 10 g/mile more stringent standards in MY 2026, on which we requested comment. In addition, during the public hearing, many of these commenters, as well as speakers who identified themselves as representing frontline communities, urged the strongest possible emissions standards to address environmental impacts on overburdened communities. There was also broad opposition among these commenters to the proposed flexibilities and incentives, based on concerns that the flexibilities were unnecessary and would compromise the stringency of the program. In addition, tens of thousands of individual public commenters echoed these themes, urging EPA to establish the strongest possible GHG emissions standards.

As discussed in Section I.B of this preamble, the final rule revises GHG emissions standards for MYs 2023-2026, incorporating several changes from the proposed standards and flexibilities, based on our consideration of the public comments and updated information and analysis. As discussed in Section I.A.2 of this preamble, it is EPA's assessment that the final standards are reasonable and appropriate, after considering lead time, cost, and other relevant factors under the CAA.

As noted in the proposed rule, EPA set previous light-duty vehicle GHG emission standards in joint rulemakings where NHTSA also established CAFE standards. EPA concluded that it was not necessary for this rulemaking to be jointly issued with the National Highway Traffic Safety Administration (NHTSA). EPA has, however, coordinated with NHTSA, both on a bilateral level as well as through the interagency review process for EPA's proposed rule and this final rule facilitated by the Office of Management and Budget (OMB) under E.O. 12866.

2. Why does EPA believe the final standards are appropriate under the CAA?

EPA is revising GHG emissions standards for passenger cars and light trucks under the authority provided by section 202(a) of the CAA. Section 202(a) requires EPA to establish standards for emissions of pollutants from new motor vehicles which, in the Administrator's judgment, cause or contribute to air pollution which may reasonably be anticipated to endanger public health or welfare. Standards under section 202(a) take effect “after such period as the Administrator finds necessary to permit the development and application of the requisite technology, giving appropriate consideration to the cost of compliance within such period.” Thus, in establishing or revising section 202(a) standards designed to reduce air pollution that endangers public health and welfare, EPA also must consider technological feasibility, compliance cost, and lead time. EPA also may consider other factors and in previous light-duty vehicle GHG standards rulemakings has considered the impacts of potential GHG standards on the auto industry, cost impacts for consumers, oil conservation, energy security and other energy impacts, as well as other relevant considerations such as safety.

When considering these factors for the SAFE rule, EPA identified several factors, primarily costs to manufacturers and upfront costs to vehicle purchasers, as disfavoring maintaining or increasing the stringency of the then-existing standards, and other factors, such as reduced emissions that endanger public health and welfare and reduced operating costs for consumers, as favoring increased stringency (or a lesser degree of reduced stringency from the then-existing standards). In balancing these factors in the SAFE rule, EPA placed greater weight on the former factors (reducing the costs for the manufacturers and reducing upfront costs for vehicle buyers), and thereby decided to make EPA's GHG standards significantly less stringent. However, the purpose of adopting standards under CAA section 202 is to address air pollution that may reasonably be anticipated to endanger public health and welfare. Indeed, reducing air pollution has traditionally been the focus of such standards.

EPA has reconsidered how costs, lead time and other factors were weighed in the SAFE rule against the potential for achieving emissions reductions and is reaching a different conclusion as to the appropriate stringency of the standards. In light of the statutory purpose of CAA section 202, the Administrator is placing greater weight on the emission reductions and resulting public health and welfare benefits and, taking into consideration EPA's updated technical analysis, accordingly is establishing significantly more stringent standards for MYs 2023-2026 compared to the standards established by the SAFE rule.

We are revising decisions made in the SAFE final rule in accordance with our updated technical analyses for the proposed and final rule. EPA's approach is consistent with Supreme Court decisions affirming that agencies are free to reconsider and revise their prior decisions where they provide a reasonable explanation for their revised decisions. 5 In this rule, the agency is changing its 2020 position and restoring its previous approach by finding, in light of its updated technical analyses and of the statutory purposes of the CAA and in particular of section 202(a), that it is more appropriate to place greater weight on the magnitude and benefits of reducing emissions that endanger public health and welfare, while continuing to consider compliance costs, lead time and other relevant factors. In addition to the greater emphasis on emissions reductions, the agency's decision to adopt more stringent standards for MYs 2023-2026 is significantly informed by consideration of new information that was not available during the SAFE rule development. Specifically, the agency's decision has been informed by the further technological advancements and successful implementations of electric vehicles since the SAFE rule, by the recent manufacturer announcements signaling an accelerated transition to electrified vehicles, and by additional evidence of sustained and active credit trading as manufacturers take advantage of this additional flexibility for adopting emissions-reducing technologies across the new vehicle fleet.

5 See, e.g., Encino Motorcars, LLC v. Navarro, 136 S. Ct. 2117, 2125 (2016); FCC v. Fox Television Stations, Inc., 556 U.S. 502, 515 (2009).

When considering these factors for the SAFE rule, EPA identified several factors, primarily costs to manufacturers and upfront costs to vehicle purchasers, as disfavoring maintaining or increasing the stringency of the then-existing standards, and other factors, such as reduced emissions that endanger public health and welfare and reduced operating costs for consumers, as favoring increased stringency (or a lesser degree of reduced stringency from the then-existing standards). In balancing these factors in the SAFE rule, EPA placed disproportionate weight on the former factors (reducing the costs for the manufacturers and reducing upfront costs for vehicle buyers), and thereby significantly diminished the relative weight given to the latter factors (increased operating costs and increased harmful emissions). The SAFE rule relied on this re-weighting to justify making EPA's GHG standards significantly less stringent in a way that (under the SAFE rule's own analysis) would have resulted in increases in CO2 emissions of 867 MMT (over the vehicles' lifetimes), increases in criteria pollutants, and resulting increases in adverse health effects (as well as net costs to public welfare). 6

6 See 85 FR 25111, April 30, 2020.

The purpose of adopting standards under CAA section 202, however, is to address air pollution that may reasonably be anticipated to endanger public health and welfare. Indeed, reducing air pollution has traditionally been the focus of such standards. EPA has therefore updated its technical analysis of potential emissions control technologies, costs and lead time and reconsidered how those and other factors were weighed in the SAFE rule against the potential for achieving emissions reductions. In light of the statutory purpose of CAA section 202, the Administrator is restoring the appropriate, central consideration given to the emission reductions from motor vehicles and resulting public health and welfare benefits, while still giving appropriate consideration to compliance costs and other factors (including savings in vehicle operating costs). Accordingly, EPA is establishing significantly more stringent standards for MYs 2023-2026 compared to the standards established by the SAFE rule.

As discussed in Section III.A of this preamble, the standards take into consideration both the updated analyses for the proposed and final rule and past EPA analyses conducted for previous GHG standards. We are revising decisions made in the SAFE final rule in accordance with Supreme Court decisions affirming that agencies are free to reconsider and revise their prior decisions where they provide a reasonable explanation for their revised decisions. In this rulemaking, the agency is changing its 2020 position and restoring its previous approach by finding, in light of the statutory purposes of the CAA and in particular of section 202(a), that it is more appropriate to place considerable weight on the magnitude and benefits of reducing emissions that endanger public health and welfare, while continuing to consider compliance costs, lead time and other relevant factors.

EPA has carefully considered the technological feasibility and cost of the full range of alternatives on which we sought public comment in the proposed rule and the available lead time for manufacturers to comply with them, including the role of flexibilities designed to facilitate compliance. In our technical assessment, discussed in further detail in section VI.A of this preamble, we conclude that there has been ongoing advancement in emissions reducing technologies since the beginning of the EPA's program in 2012, and that there is potential for greater penetration of these technologies across all new vehicles. In addition to improvements in ICE vehicles, recent advancements in electric vehicle technologies have greatly increased the available options for manufacturers to meet more stringent standards. Based on our updated technical analyses and consideration of the public comments, EPA has determined that standards that are more stringent in the later model years (i.e., after MY 2024) than the proposed standards are more appropriate under Section 202(a).

In recognition of lead time considerations, for MYs 2023 and 2024, EPA is finalizing the proposed standards for those model years. For MYs 2025 and 2026, EPA has determined that it is appropriate to finalize standards more stringent than those proposed, and, as described in more detail in section I.B of this preamble, we are finalizing standards that are the most stringent of the alternatives considered in the proposed rule for those model years.

This approach best meets EPA's responsibility under the CAA to protect human health and the environment, as well as its statutory obligation to consider lead time, feasibility, and cost. The final standards will result in significantly greater reductions of GHG emissions over time compared to the proposed standards. EPA projects that the final standards will result in a reduction of 3.1 billion tons of GHG emissions by 2050—50 percent greater emission reductions than our proposed standards. In addition, the final standards will reduce emissions of some criteria pollutants and air toxics, resulting in important public health benefits, as described in Section V of this preamble. The final standards will result in reduced vehicle operating costs for consumers. The fuel consumption reduced by the final standards will save consumers $210 to $420 billion in retail fuel costs through 2050. Although the up-front technology cost for a MY 2026 vehicle meeting the final standards is estimated to be $1,000 on average, drivers will recover that up-front cost over time through savings in fuel costs. For an individual consumer on average, EPA estimates that, over the lifetime of a MY 2026 vehicle, the reduction in fuel costs will exceed the increase in vehicle costs by $1,080 (see Section VII.J of this preamble). Further, the overall benefits of the program will far outweigh the costs, as EPA estimates net benefits of $120 billion to $190 billion through 2050. 7 Section I.B of this preamble describes the final standards in more detail.

7 See Section VII.I of this preamble for more detail.

In developing this final rulemaking, EPA updated the analyses based, in part, on our assessment of the public comments. We agree with commenters who stated that it is appropriate to update certain key inputs—for example, the vehicle baseline fleet and certain technology costs—to reflect newer data. For example, a key update was to the estimates of battery costs for electrified vehicles, which have decreased significantly in recent years. EPA's approach to updating these costs and other inputs to the analyses is described in Section III.A of this preamble.

The more stringent standards for MY 2025 and 2026 also provide a more appropriate transition to new standards for MY 2027 and beyond. As stated in the proposal, EPA is planning to initiate a rulemaking to establish multi-pollutant emission standards for MY 2027 and later (see the preamble to the proposed rule at section I.A.3). Consistent with the direction of Executive Order 14037, “Strengthening American Leadership in Clean Cars and Trucks,” 8 this subsequent rulemaking will extend to at least MY 2030 and will apply to light-duty vehicles as well as medium-duty vehicles (e.g., commercial pickups and vans, also referred to as heavy-duty class 2b and 3 vehicles) and is likely to significantly build upon the standards established in this final rule. EPA looks forward to engaging with all stakeholders, including states and our federal partners, to inform the development of these future standards.

8 86 FR 43583, August 10, 2021.

B. Summary of Final Light-Duty Vehicle GHG Program

EPA is finalizing revised GHG standards that begin in MY 2023 and increase in stringency year over year through MY 2026.

After consideration of public comments, EPA is adopting the following approach for setting the final standards:

- For MYs 2023 and 2024, EPA is finalizing the proposed standards.

- For MY 2025, EPA is finalizing the Alternative 2 standards (the most stringent standards considered in the proposed rule for this MY).

- For MY 2026, EPA is finalizing the most stringent alternative upon which we sought comment—the Alternative 2 standards with an additional 10 g/mile increased stringency.

EPA is finalizing optional flexibility provisions for manufacturers that are more targeted than proposed, primarily to focus most of the flexibilities on MYs 2023-2024 in consideration of lead time for manufacturers and to help them manage the transition to more stringent standards by providing some additional flexibility. We summarize the final flexibility program elements, including an analysis of key public comments, in Sections II.A.4 and II.B of this preamble.

This final rule accelerates the rate of stringency increases of the MY 2023-2026 SAFE standards from a roughly 1.5 percent year-over-year rate of stringency increase to a nearly 10 percent stringency increase from MY 2022 to MY 2023, followed by a 5 percent stringency increase in MY 2024, as proposed. In MY 2025, the stringency of the final standards increases by 6.6 percent, culminating with a 10 percent stringency increase in MY 2026, as provided in the Alternative 2 standards with an additional 10 g/mile increased stringency in MY 2026, on which we sought comment.

EPA believes the 10 percent increase in stringency in MY 2023 is appropriate given the technological investments industry was on track to make under the 2012 standards and has continued to make beyond what would be required to meet the SAFE rule standards, as well as the compliance flexibilities available within the program. This is illustrated in part by several manufacturers, representing nearly 30 percent of the nationwide auto market, having chosen to participate in the California Framework Agreements. Our decision to finalize the more stringent Alternative 2 standards for MY 2025, and the Alternative 2 standards with a further increase of stringency of 10 g/mile in MY 2026 takes into account the additional lead time available for MYs 2025-2026 compared to MYs 2023-2024. Given this additional lead time, EPA has determined that it is appropriate, particularly in light of the accelerating transition to electrified vehicles that has already begun, to require additional emissions reductions in this time frame. The resulting trajectory of increasing stringency from MYs 2023 to 2026 also takes into account the credit-based emissions averaging, banking and trading flexibilities of the current program, including flexibility provisions that have been retained, and the targeted additional flexibilities that are being extended in this final rule, especially in the early years of the program. EPA has also taken into account manufacturers' ability to generate credits against the existing standards that were relaxed in the SAFE rule for MYs 2021 and 2022, which we are not revising. The final standards for MYs 2023-2026 will achieve significant GHG and other emission reductions and related public health and welfare benefits, while providing consumers with lower operating costs resulting from significant fuel savings. Our analyses described in this final rule support the conclusion that the final standards are appropriate under section 202(a) of the CAA, considering costs, technological feasibility, available lead time, and other factors.

In our design and analyses of the final program, and our overall updated assessment of feasibility, EPA took into account the decade-long light-duty vehicle GHG emission reduction program in which the auto industry has introduced a wide lineup of ever more fuel-efficient, GHG-reducing technologies that are already present in much of the fleet and will enable the industry to achieve the standards established in this rule. As explained in the preamble to the proposed rule, in light of the design cycle timing for manufacturers of light-duty vehicles, EPA reasonably expects that the vehicles that automakers will be selling during the first years of the MY 2023-2026 program were already designed before the less stringent SAFE standards were adopted.

Most automakers have launched ambitious plans to develop and produce increasing numbers of zero- and near-zero-emission vehicles. EPA recognizes that during the near-term timeframe of the standards, the new vehicle fleet likely will continue to consist predominantly of gasoline-fueled vehicles, although the volumes of electrified vehicles will continue to increase, particularly in MYs 2025 and 2026. In this preamble and the Regulatory Impact Analysis (RIA), we provide analyses supporting our assessment that the final standards for MYs 2023 through 2026 are achievable primarily through the application of advanced gasoline vehicle technologies but with a growing percentage of electrified vehicles. We project that during the four-year ramp up of the stringency of the GHG standards, the standards can be met with gradually increasing sales of plug-in electric vehicles in the U.S., from about 7 percent market share in MY 2023 (including both fully electric vehicles (EVs) and plug-in hybrid vehicles (PHEVs)) up to about 17 percent in MY 2026. In MY 2020, EVs and PHEVs represented about 2.2 percent of U.S. new vehicle production. 9 From January through September 2021, EVs and PHEVs represented 3.6 percent of total U.S. light-duty vehicle sales, 10 and are projected to be 4.1 percent of production by the end of MY 2021. 11 This rule is expected to result in an increase in penetration of EV and PHEV vehicles from today's levels, and we believe the projected penetrations are reasonable when considering the results of our analysis as well as these trends in the growth of EV market share, as well as the proliferation of recent automaker announcements on plans to transition toward an electrified fleet (which we discuss in Section III.C of this preamble). Projections of future EV market share also increasingly show rates of EV penetration commensurate with what we project under the final standards. 12 13 14 Numerous automaker announcements of a rapidly increasing focus on EV and PHEV production (see Section III.C of this preamble), which were reiterated in their public comments, show that automakers are already preparing for rapid growth in EV penetration. EPA finds that, given the rate and breadth of these announcements across the industry, the levels of EV penetration we project to occur are appropriate. As described elsewhere in this preamble, based on our analysis of the final standards, we believe that the targeted incentives and flexibilities that we are finalizing for the early years of the program will further address lead time considerations as well as support the acceleration of automakers' introduction and sales of advanced technologies, including zero and near-zero-emission technologies.

9 “The 2021 EPA Automotive Trends Report, Greenhouse Gas Emissions, Fuel Economy, and Technology since 1975,” EPA-420R-21023, November 2021.

10 Argonne National Laboratory, “Light Duty Electric Drive Vehicles Monthly Sales Updates,” September 2021, accessed on October 20, 2021 at: https://www.anl.gov/es/light-duty-electric-drive-vehicles-monthly-sales-updates.

11 “The 2021 EPA Automotive Trends Report, Greenhouse Gas Emissions, Fuel Economy, and Technology since 1975,” EPA-420R-21023, November 2021.

12 Bloomberg New Energy Finance (BNEF), BNEF EV Outlook 2021, Figure 5. Accessed on November 1, 2021 at https://about.bnef.com/electric-vehicle-outlook/ (Figure 5 indicates U.S. BEV+PHEV penetrations of approximately 7% in 2023, 9% in 2024,11% in 2025 and 15% in 2026).

13 IHS Markit, “US EPA Proposed Greenhouse Gas Emissions Standards for Model Years 2023-2026; What to Expect,” August 9, 2021. Accessed on October 28, 2021 at https://ihsmarkit.com/research-analysis/us-epa-proposed-greenhouse-gas-emissions-standards-MY2023-26.html (Table indicates 12.2% in 2023, 16% in 2024, 20.1% in 2025 and 24.3% in 2026).

14 Rhodium Group, “Pathways to Build Back Better: Investing in Transportation Decarbonization,” May 13, 2021. Accessed on November 1, 2021 at https://rhg.com/research/build-back-better-transportation/ (Figure 3 indicates EV penetration of 11% to 19% in 2026 under a current policy scenario).

We describe additional details of the final standards below and in later sections of the preamble as well as in the RIA.

1. Final Revised GHG Emissions Standards

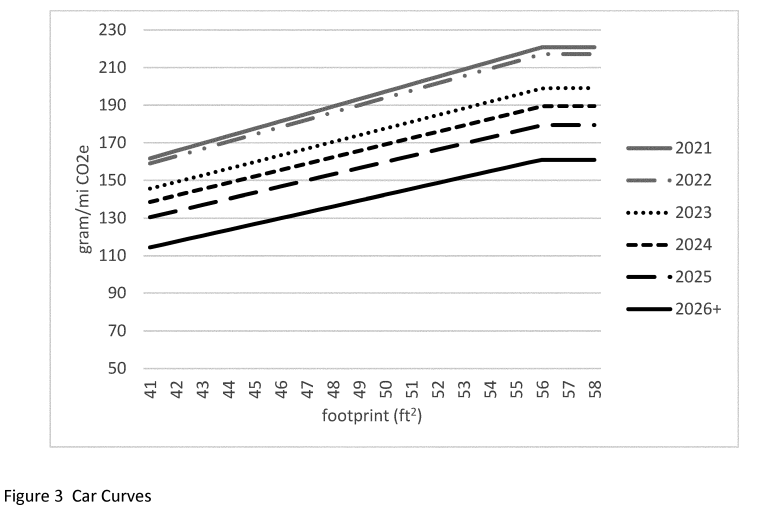

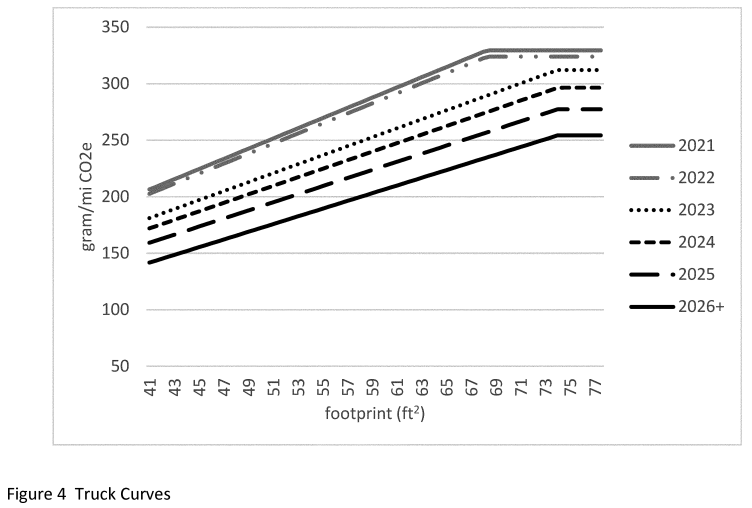

As with EPA's previous light-duty GHG programs, as proposed, EPA is finalizing footprint-based standards curves for both passenger cars and light trucks (throughout this action, “trucks” or “light trucks” refers to light-duty trucks). Each manufacturer has a unique standard for the passenger cars category and another for the truck category 15 for each MY based on the sales-weighted footprint-based CO2 targets 16 of the vehicles produced in that MY.

15 Passenger cars include cars and smaller cross-overs and SUVs, while the truck category includes larger cross-overs and SUVs, minivans, and pickup trucks.

16 Because compliance is based on the full range of vehicles in a manufacturer's car and truck fleets, with lower-emitting vehicles compensating for higher-emitting vehicles, the emission levels of specific vehicles within the fleet are referred to as targets, rather than standards.

EPA is finalizing the proposed standards for MYs 2023 and 2024, the Alternative 2 standards for MY 2025, and the Alternative 2 standards minus 10 g/mile for MY 2026. In the proposed rule, EPA requested comment on standards for MY 2026 that would result in fleet average target levels that are in the range of 5-10 g/mile lower (i.e., more stringent) than the levels proposed in each of the three alternatives, and is finalizing a level 10 g/mile lower than the proposed rule's Alternative 2 for MY 2026.

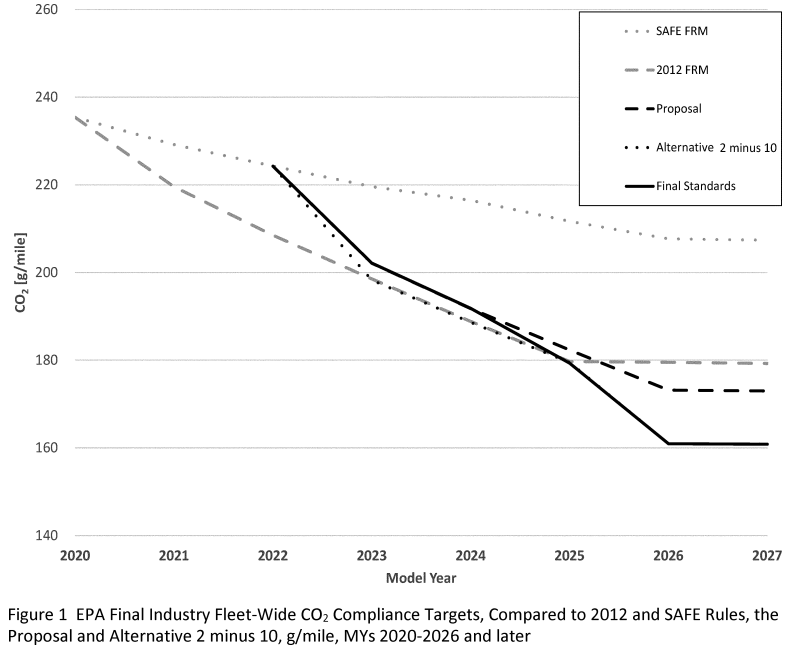

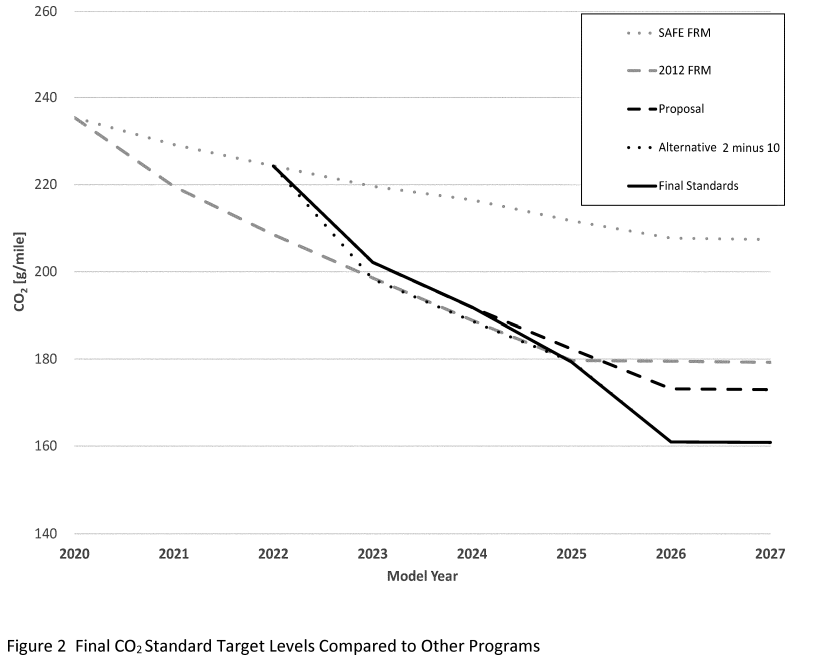

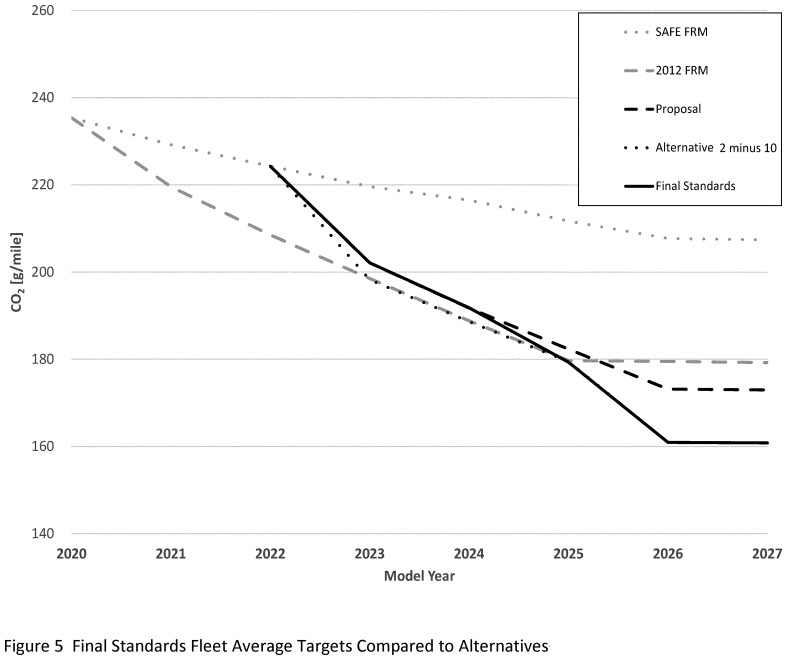

Figure 1 shows EPA's final standards, expressed as average projected fleetwide GHG emissions targets (cars and trucks combined), through MY 2026. For comparison, the figure also shows the corresponding targets for the proposed standards (Proposal), the Alternative 2 standards reduced by 10 g/mile in MY 2026 (Alternative 2 minus 10), as described further in Section II.C of this preamble, the SAFE standards, and the 2012 FRM standards. 17 The projected fleet targets for the final standards increase in stringency in MY 2023 by almost 10 percent (compared to the SAFE rule standards in MY 2022), followed by stringency increases of 5 percent in MY 2024, 6.6 percent in MY 2025 and 10 percent in MY 2026. As with all EPA vehicle emissions standards, the MY 2026 standards will remain in place for all subsequent MYs, unless and until the standards for future MYs are revised in a subsequent rulemaking. As noted previously, EPA is planning a future rulemaking to establish new emissions standards for MY 2027 and beyond.

17 The Proposal and Alternative 2 minus 10 standards are the less and more stringent alternatives EPA analyzed in addition to the final rule. See Sections II.C and III.D of this preamble for more information these alternatives.

Table 1 presents the projected overall industry fleetwide CO2 -equivalent emission compliance target levels, based on EPA's final standards presented in Figure 1. The industry fleet-wide estimates in Table 1 are projections based on EPA's modeling, taking into consideration projected fleet mix and footprints for each manufacturer's fleet in each model year. Table 2 presents projected industry fleet average year-over-year percent reductions (and cumulative reductions from 2022 through 2026) comparing the standards under the SAFE rule and the revised final standards. See Section II.A of this preamble for a full discussion of the final standards and presentations of the footprint standards curves.

BILLING CODE 6560-50-P

BILLING CODE 6560-50-C

| Model year | Cars CO2 (g/mile) | Light trucks CO2 (g/mile) | Fleet CO2 (g/mile) |

|---|---|---|---|

| * The combined car/truck CO 2 targets are a function of projected car/light truck shares, which have been updated for this final rule (MY 2020 is 44 percent car and 56 percent light trucks while the projected mix changes to 47 percent cars and 53 percent light trucks by MY 2026). | |||

| 2022 (SAFE reference) | 181 | 261 | 224 |

| 2023 | 166 | 234 | 202 |

| 2024 | 158 | 222 | 192 |

| 2025 | 149 | 207 | 179 |

| 2026 and later | 132 | 187 | 161 |

| Total change 2022-2026 | −49 | −74 | −63 |

| * Note the percentages shown for the SAFE rule targets have changed slightly from the proposed rule, due to the updates in our base year fleet from MY 2017 to MY 2020 manufacturer fleet data. | |||||||||

| ** These are modeled results based on projected fleet characteristics and represent percent reductions in projected targets, not the standards (which are the footprint car/truck curves), associated with that projected fleet (see Section III of this preamble for more detail on our modeling results). | |||||||||

| SAFE rule standards * | Proposed standards ** | Final standards ** | |||||||

| Cars (%) | Trucks (%) | Combined (%) | Cars (%) | Trucks (%) | Combined (%) | Cars (%) | Trucks (%) | Combined (%) | |

| 2023 | 1.7 | 1.7 | 2.1 | 8.4 | 10.4 | 9.8 | 8.4 | 10.4 | 9.8 |

| 2023 | 1.7 | 1.7 | 2.1 | 8.4 | 10.4 | 9.8 | 8.4 | 10.4 | 9.8 |

| 2024 | 0.6 | 1.5 | 1.4 | 4.7 | 5.0 | 5.1 | 4.8 | 4.9 | 5.1 |

| 2025 | 2.3 | 1.7 | 2.2 | 4.8 | 5.0 | 5.0 | 5.7 | 7.0 | 6.6 |

| 2026 | 1.8 | 1.6 | 1.9 | 4.8 | 5.0 | 5.0 | 11.4 | 9.5 | 10.3 |

| Cumulative | 6.3 | 6.3 | 7.4 | 20.9 | 23.1 | 22.8 | 27.1 | 28.3 | 28.3 |

2. Final Compliance Flexibilities and Advanced Technology Incentives

EPA received many comments on the proposed flexibility provisions. After considering the comments along with our updated analyses, we are finalizing flexibility provisions that are narrower than proposed in several aspects, primarily to focus the additional flexibilities in MYs 2023-2024 to help manufacturers manage the transition to more stringent standards by providing some additional flexibility in the near-term. We summarize the final flexibility program elements, including a summary and analysis of key comments, in Section II.B of this preamble.

EPA proposed a set of extended or additional temporary compliance flexibilities and incentives that we believed would be appropriate given the stringency and lead time of the proposed standards. We proposed four types of flexibilities/incentives, in addition to those already available under EPA's previously established regulations: (1) A limited extension of carry-forward credits generated in MYs 2016 through 2020 beyond the normal five years otherwise specified in the regulations; (2) an extension of the advanced technology vehicle multiplier credits for MYs 2022 through 2025 with a cumulative credit cap; (3) full-size pickup truck incentives for strong hybrids or similar performance-based credit for MYs 2022 through 2025 (provisions which were removed in the SAFE rule); and (4) an increase of the off-cycle credits menu cap from 10 g/mile to 15 g/mile. EPA also proposed to remove the multiplier incentives for natural gas fueled vehicles for MYs 2023-2026.

The GHG program includes existing provisions initially established in the 2010 rule, which set the MYs 2012-2016 GHG standards, for how credits may be used within the program. These averaging, banking, and trading (ABT) provisions include credit carry-forward, credit carry-back (also called deficit carry-forward), credit transfers (within a manufacturer), and credit trading (across manufacturers). These ABT provisions define how credits may be used and are integral to the program, essentially enabling manufacturers to plan compliance over a multi-year time period. The current program allows credits to be carried forward for 5 years (i.e., a 5-year credit life). EPA proposed a two-year extension of MYs 2016 credit life and a one-year extension of MYs 2017-2020 credit life.

EPA is finalizing a more limited approach to credit life extension, adopting only a one-year extension for MY 2017-2018 credits, as shown in Table 3 below. EPA was persuaded by public comments from non-governmental organizations (NGOs), some states including California, and EV manufacturers that the proposed credit life extension overall was unnecessary and could diminish the stringency of the final standards. While several auto industry commenters suggested even additional credit life extensions, EPA's assessment is that the standards are feasible with the more narrowed credit extensions of one-year for the MYs 2017 and 2018 credits, which make more credits available in the early years of the program, MYs 2023 and 2024, to help manufacturers manage the transition to more stringent standards by providing some additional flexibility. For all other credits generated in MY 2016 and later, credit carry-forward remains unchanged at five years.

| x = Previous program. + = Additional years included in Final Rule. | |||||||||||

| MY credits are banked | MYs credits are valid under extension | ||||||||||

| 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | 2026 | |

| 2016 | x | x | x | x | x | ||||||

| 2017 | x | x | x | x | x | + | |||||

| 2018 | x | x | x | x | x | + | |||||

| 2019 | x | x | x | x | x | ||||||

| 2020 | x | x | x | x | x | ||||||

| 2021 | x | x | x | x | x | ||||||

The previous GHG program also includes temporary incentives through MY 2021 that encourage the use of advanced technologies such as electric, hybrid, and fuel cell vehicles, as well as incentives for full-size pickups using strong hybridization or technologies providing similar emissions reductions to hybrid technology. The full-size pickup incentives originally (in the 2012 rule) were available through MY 2025, but the SAFE rule removed these incentives for MYs 2022 through 2025. When EPA established these incentives in the 2012 rule, EPA recognized that they would reduce the effective stringency of the standards, but believed that it was worthwhile to have a limited near-term loss of emissions reduction benefits to increase the potential for far greater emissions reduction and technology diffusion benefits in the longer term. 18 EPA believed that the temporary regulatory incentives would help bring low emission technologies to market more quickly than an effective market would in the absence of incentives. 19 20 With these same goals in mind for this program, EPA proposed multiplier incentives from MYs 2022 through MY 2025 with a cap on multiplier credits and to reinstate the full-size pickup incentives also for MYs 2022 through 2025. The proposed incentives were intended as a temporary measure supporting the transition to zero-emission vehicles and to provide additional flexibility in meeting the MY 2023-2026 proposed standards.

18 See Tables III-2 and III-3, 77 FR 62772, October 15, 2012.

19 77 FR 62812, October 15, 2012.

20 Manufacturers use of the incentives is provided in “The 2021 EPA Automotive Trends Report, Greenhouse Gas Emissions, Fuel Economy, and Technology since 1975,” EPA-420R-21023, November 2021.

However, EPA is finalizing a narrower timeframe for the temporary multiplier and full-size pickup incentives, focusing the incentives only in MYs 2023-2024, to help manufacturers manage the transition to more stringent standards by providing some additional flexibility. After considering comments and further analyzing the potential impact of multipliers on costs and emissions reductions, EPA is adopting temporary multipliers for MYs 2023-2024 at a level lower than proposed while finalizing the proposed credit cap of 10 g/mile cumulatively, as further discussed in Section II.B.1 of this preamble. EPA is not finalizing multiplier incentives for MY 2022 or MY 2025 and is instead sunsetting them at the end of MY 2024. Under this approach, manufacturers utilizing this optional incentive program would need to produce more advanced technology vehicles (EVs, PHEVs or fuel cells) in order to fully utilize multiplier credits before reaching the cap, thus incentivizing greater volumes of these zero and near-zero emission vehicles. Similarly, EPA is finalizing temporary full-size pickup incentives only for MYs 2023-2024 and sunsetting them at the end of MY 2024. These provisions are further discussed in Section II.B.2 of this preamble.

EPA is finalizing our proposed removal of the extended multiplier incentives for natural gas vehicles (NGVs) after MY 2022, which was added by the SAFE rule, because NGVs are not a near-zero emissions technology and EPA believes multipliers are no longer necessary or appropriate for these vehicles. NGV multiplier incentives are discussed in Section II.B.1.iii of this preamble.

For the off-cycle credits program, EPA is finalizing our proposed incentive to increase the menu cap from 10 to 15 g/mile, but for a more limited time frame. EPA is finalizing this cap increase beginning in MY 2023 through MY 2026, instead of beginning the cap increase in MY 2020 as in the proposed rule. Off-cycle credits are intended to reflect real-world emissions reductions for technologies not captured on the CO2 compliance test cycles. EPA agrees with public comments from many NGOs and states that increasing the off-cycle credit menu cap starting in MY 2020 would unnecessarily provide additional credit opportunities during the years of the weakened SAFE standards in MYs 2021 and 2022. EPA also is finalizing revised definitions for three off-cycle technologies to begin in MY 2023, to ensure real-world emission reductions consistent with the menu credit values. See Section II.B.3 of this preamble for further information.

C. Analytical Support for the Final Revised Standards

EPA updated several key inputs to our analysis for this final rule based on public comments and newer available data, as detailed in Section III.A of this preamble, including updates to the baseline vehicle fleet and battery costs, issues on which we received a substantial number of public comments.

We have updated the baseline vehicle fleet to reflect the MY 2020 fleet rather than the MY 2017 fleet used in the analysis for the proposed rule. 21 As a result, there is slightly more GHG-reducing technology contained in the baseline fleet and the fleet mix has changed to reflect more light trucks in the fleet (56 percent trucks/44 percent cars, compared to the 50/50 car/truck split in the analysis for the proposed rule).

21 EPA's updated MY 2020 baseline fleet is generally consistent with that used by NHTSA in their recent CAFE NPRM (86 FR 49602, September 3, 2021).

In the proposed rule, we noted that the electrified vehicle battery costs used in the SAFE FRM, which were carried over to the proposed rule analysis, could be lower based on EPA's latest assessment and that updating those costs for the proposed rule would not have had a notable impact on overall cost estimates. This conclusion was based in part on our expectation that electrification would continue to play a relatively modest role in our projections of compliance paths for the proposed standards, as it had in all previous analyses of standards with a similar level of stringency. We also noted in the proposal that we could update battery costs for the final rule and requested comment on whether our choice of modeling inputs such as these should be modified for the final rule analysis. In response to the public comments regarding EPA's battery cost estimates used in the proposed rule, EPA has updated the battery costs for the final rule analysis based on the most recent available data, resulting in lower projected battery costs compared to our proposed rule. EPA agrees with commenters that battery costs used in the proposed rule were higher than recent evidence supports. Consideration of the current costs of batteries for electrified vehicles, as widely reported in the trade and academic literature and further supported by our battery cost modeling tools, led EPA to adjust the battery costs to more accurately account for these trends. Based on an updated assessment, described further in Section III.A of this preamble and Chapter 2 of the RIA, we determined that battery costs should be reduced by about 25 percent. More information on the public comments we received and the revised inputs leading to this change is available in Section III.A of this preamble and Chapter 2 of the RIA.

Other key changes to our analysis since the proposed rule include:

- Updated projections from EIA (AEO 2021), including Gross Domestic Product, number of households, vehicle miles traveled (VMT) growth rates and historic fleet data

- Updated energy security cost per gallon factors

- Updated tailpipe and upstream emission factors

- High compression ratio level 2 (HCR2) technology was removed as a separate compliance option within the model although HCR0 and HCR1 remain as options 22 23

22 For further details on HCR definitions, see Chapter 2.3.2 of the RIA. For HCR implementation in CCEMS, see Chapter 4.1.1.3 of the RIA.

23 See Section III.A of this preamble.

- Increased utilization of BEVs with a 300 mile range and lower utilization of BEVs with a 200 mile range

- Updated credit banks reflecting more recent information from EPA's manufacturer certification and compliance data

- Updated valuation of off-cycle credits (lower costs) and updated assumptions for off-cycle credit usage across manufacturers

- Updated vehicle sales elasticity (changed from −1 percent to −0.4 percent) based on a recent EPA study 24

24 See Section VII.B of this preamble.

More information on these and other analysis updates is in Section III.A of this preamble.

As with our earlier analyses, including SAFE and the August 2021 EPA proposed rule, for this final rule EPA used a model to simulate the decision process of auto manufacturers in choosing among the emission reduction technologies available to incorporate in vehicles across their fleets. The model takes into account both the projected costs of technologies and the relative ability of each of these technologies to reduce GHG emissions. This process identifies potential pathways for manufacturers to comply with a given set of GHG standards. EPA then estimates projected average and total costs for manufacturers to produce these vehicles to meet the standards under evaluation during the model years covered by the analysis.

In addition to projecting the technological capabilities of the industry and estimating compliance costs for each of the four affected model years (MYs 2023-2026), EPA has considered the role of the averaging, banking, and trading system that has been available and extensively used by the industry since the beginning of the light-duty vehicle GHG program in model year 2012. Our analysis of the current and anticipated near-future usage of the GHG credit mechanisms reinforces the trends we identified in our other analyses showing widespread technological advancement in the industry at reasonable per-vehicle costs. Together, these analyses support EPA's conclusion under section 202(a) of the CAA that technologically feasible pathways are available at reasonable costs for automakers to comply with EPA's standards during each of the four model years. We discuss these analyses and their results further in Section III of this preamble.

We also estimate the GHG and non-GHG emission impacts (tailpipe and upstream) of the standards. EPA then builds on the estimated changes in emissions and fuel consumption to calculate projected net economic impacts from these changes. Key economic inputs include: Measures of health impacts from changes in criteria pollutant emissions; a value for the vehicle miles traveled “rebound effect;” estimates of energy security impacts of changes in fuel consumption; the social costs of GHGs; and costs associated with crashes, noise, and congestion from additional rebound driving.

Our overall analytical approach generates key results for the following metrics: Incremental costs per vehicle (industry-wide averages and by manufacturer); total vehicle technology costs for the auto industry; GHG emissions reductions and criteria pollutant emissions reductions; penetration of key GHG-reducing technologies across the fleet; consumer fuel savings; oil reductions; and net societal costs and benefits. We discuss these analyses in Sections III, IV, V, and VII of this preamble as well as in the RIA.

D. Summary of Costs, Benefits and GHG Emission Reductions of the Final Program

EPA estimates that the total benefits of this final rule far exceed the total costs—the net present value of benefits is between $120 billion to $190 billion (annualized net benefits between $6.2 billion to $9.5 billion). Table 4 below summarizes EPA's estimates of total discounted costs, fuel savings, and benefits. The results presented here project the monetized environmental and economic impacts associated with the final program during each calendar year through 2050.

The benefits include climate-related economic benefits from reducing emissions of GHGs that contribute to climate change, reductions in energy security externalities caused by U.S. petroleum consumption and imports, the value of certain particulate matter-related health benefits, the value of additional driving attributed to the rebound effect, and the value of reduced refueling time needed to fill a more fuel-efficient vehicle. Between $8 and $19 billion of the total benefits through 2050 are attributable to reduced emissions of non-GHG pollutants, primarily those that contribute to ambient concentrations of smaller particulate matter (PM2.5 ). PM2.5 is associated with premature death and serious health effects such as hospital admissions due to respiratory and cardiovascular illnesses, nonfatal heart attacks, aggravated asthma, and decreased lung function. The program will also have other significant social benefits including $130 billion in climate benefits (with the average SC-GHGs at a 3 percent discount rate) and fuel savings of $150 billion to $320 billion exclusive of fuel taxes. For American drivers, who purchase fuel inclusive of fuel taxes, the fuel savings will total $210 billion to $420 billion through 2050 (see Table 44). With these fuel savings, consumers will benefit from reduced operating costs over the vehicle lifetime. Over the lifetime of a MY 2026 vehicle, EPA estimates that the reduction in fuel costs will exceed the increase in vehicle costs by $1,080 for consumers on average.

The analysis also includes estimates of economic impacts stemming from additional vehicle use from increased rebound driving, such as the economic damages caused by crashes, congestion, and noise. See Chapter 3 of the RIA for more information regarding these estimates.

| Notes: | ||||

| a Values rounded to two significant figures; totals may not sum due to rounding. Present and annualized values are based on the stream of annual calendar year costs and benefits included in the analysis (2021-2050) and discounted back to year 2021. | ||||

| b Climate benefits are based on reductions in CO 2 , CH 4 and N 2 O emissions and are calculated using four different estimates of the social cost of each GHG (SC-GHG model average at 2.5%, 3%, and 5% discount rates; 95th percentile at 3% discount rate), which each increase over time. In this table, we show the benefits associated with the average SC-GHGs at a 3% discount rate but the Agency does not have a single central SC-GHG point estimate. We emphasize the importance and value of considering the benefits calculated using all four SC-GHG estimates and present them later in this preamble. As discussed in Chapter 3.3 of the RIA, a consideration of climate benefits calculated using discount rates below 3 percent, including 2 percent and lower, is also warranted when discounting intergenerational impacts. For further discussion of how EPA accounted for these estimates, please refer to section VI of this preamble and the separate Response to Comments. | ||||

| c The same discount rate used to discount the value of damages from future GHG emissions (SC-GHGs at 5, 3, and 2.5 percent) is used to calculate the present and annualized values of climate benefits for internal consistency, while all other costs and benefits are discounted at either 3% or 7%. | ||||

| d Net benefits reflect the fuel savings plus benefits minus costs. | ||||

| e Non-GHG impacts associated with the standards presented here do not include the full complement of health and environmental effects that, if quantified and monetized, would increase the total monetized benefits. Instead, the non-GHG benefits are based on benefit-per-ton values that reflect only human health impacts associated with reductions in PM 2.5 exposure. | ||||

| Present value | Annualized value | |||

| 3% discount rate | 7% discount rate | 3% discount rate | 7% discount rate | |

| Costs | $300 | $180 | $15 | $14 |

| Fuel Savings | 320 | 150 | 16 | 12 |

| Benefits | 170 | 150 | 8.6 | 8.1 |

| Net Benefits | 190 | 120 | 9.5 | 6.2 |

EPA estimates the average per-vehicle cost to meet the standards to be $1,000 in MY 2026, as shown in Table 5 below. Note that compared to the proposal, the total costs through 2050, shown in Table 4, are somewhat higher, while the per-vehicle costs shown in Table 5 are slightly lower. We discuss this in more detail in Section III.B.2 of this preamble and RIA Chapter 4.1.3.

| 2023 | 2024 | 2025 | 2026 | |

|---|---|---|---|---|

| Car | $150 | $288 | $586 | $596 |

| Light Truck | 485 | 732 | 909 | 1,356 |

| Fleet Average | 330 | 524 | 759 | 1,000 |

The final standards will achieve significant reductions in GHG emissions. As seen in Table 6 below, through 2050 the program will achieve more than 3.1 billion tons of GHG emission reductions, which is 50 percent greater emissions reductions than EPA's proposed standards.

| Emission impacts relative to no action | Percent change from no action | ||||

|---|---|---|---|---|---|

| CO 2 (million metric tons) | CH 4 (metric tons) | N 2 O (metric tons) | CO 2 | CH 4 | N 2 O |

| −3,125 | −3,272,234 | −96,735 | −9% | −8% | −8% |

E. How has EPA considered environmental justice in this final rule?

Executive Order 12898 (59 FR 7629, February 16, 1994) establishes federal executive policy on environmental justice. It directs federal agencies, to the greatest extent practicable and permitted by law, to make achieving environmental justice part of their mission by identifying and addressing, as appropriate, disproportionately high and adverse human health or environmental effects of their programs, policies, and activities on minority populations and low-income populations in the United States (U.S.). EPA defines environmental justice as the fair treatment and meaningful involvement of all people regardless of race, color, national origin, or income with respect to the development, implementation, and enforcement of environmental laws, regulations, and policies. 25

25 Fair treatment means that “no group of people should bear a disproportionate burden of environmental harms and risks, including those resulting from the negative environmental consequences of industrial, governmental and commercial operations or programs and policies.”. Meaningful involvement occurs when “(1) potentially affected populations have an appropriate opportunity to participate in decisions about a proposed activity [e.g., rulemaking] that will affect their environment and/or health; (2) the public's contribution can influence [the EPA's rulemaking] decision; (3) the concerns of all participants involved will be considered in the decision-making process; and (4) [the EPA will] seek out and facilitate the involvement of those potentially affected” A potential EJ concern is defined as “the actual or potential lack of fair treatment or meaningful involvement of minority populations, low-income populations, tribes, and indigenous peoples in the development, implementation and enforcement of environmental laws, regulations and policies.” See “Guidance on Considering Environmental Justice During the Development of an Action.” Environmental Protection Agency, https://www.epa.gov/environmentaljustice/guidance-considering-environmental-justice-during-development-action. See also https://www.epa.gov/environmentaljustice.

Executive Order 14008 (86 FR 7619, February 1, 2021) also calls on federal agencies to make achieving environmental justice part of their respective missions “by developing programs, policies, and activities to address the disproportionately high and adverse human health, environmental, climate-related and other cumulative impacts on disadvantaged communities, as well as the accompanying economic challenges of such impacts.” It declares a policy “to secure environmental justice and spur economic opportunity for disadvantaged communities that have been historically marginalized and overburdened by pollution and under-investment in housing, transportation, water and wastewater infrastructure and health care.”

Under E.O. 13563, federal agencies may consider equity, human dignity, fairness, and distributional considerations in their regulatory analyses, where appropriate and permitted by law.

EPA's 2016 “Technical Guidance for Assessing Environmental Justice in Regulatory Analysis” provides recommendations on conducting the highest quality analysis feasible, recognizing that data limitations, time and resource constraints, and analytic challenges will vary by media and regulatory context. 26

26 “Technical Guidance for Assessing Environmental Justice in Regulatory Analysis.” Epa.gov , Environmental Protection Agency, https://www.epa.gov/sites/production/files/2016-06/documents/ejtg_5_6_16_v5.1.pdf. (June 2016).

EPA's mobile source regulatory program has historically reduced significant amounts of both GHG and non-GHG pollutants to the benefit of all U.S. residents, including populations that live near roads and in communities with environmental justice (EJ) concerns. EJ concerns may arise in the context of this rulemaking in two key areas.

First, people of color and low-income populations may be especially vulnerable to the impacts of climate change. As discussed in Section IV.C of this preamble, this rulemaking will mitigate the impacts of climate change by achieving significant GHG emission reductions, which will benefit populations that may be especially vulnerable to various forms of damages associated with climate change.

Second, in addition to significant climate-change benefits, the standards will also impact non-GHG emissions. As discussed in Section VII.L.2 of this preamble, numerous studies have found that environmental hazards such as air pollution are more prevalent in areas where people of color and low-income populations represent a higher fraction of the population compared with the general population. There is substantial evidence, for example, that people who live or attend school near major roadways are more likely to be of a non-White race, Hispanic ethnicity, and/or low socioeconomic status (see Section VII.L.2 of this preamble).

We project that this rule will, over time, result in reductions of non-GHG tailpipe emissions and emissions from upstream refinery sources. We also project that the rule will result in small increases of non-GHG emissions from upstream Electric Generating Unit (EGU) sources. Overall, there are substantial PM2.5 -related health benefits associated with the non-GHG emissions reductions that this rule will achieve. The benefits from these emissions reductions, as well as the adverse impacts associated with the emissions increases, could potentially impact communities with EJ concerns, though not necessarily immediately and not equally in all locations. The air quality information needed to perform a quantified analysis of the distribution of such impacts was not available for this rulemaking. We therefore recommend caution when interpreting these broad, qualitative observations.

As noted previously, EPA intends to develop a subsequent rule to control emissions of GHGs as well as criteria and air toxic pollutants from light- and medium-duty vehicles for MYs 2027 and beyond. We are considering how to project air quality impacts from the changes in non-GHG emissions for that future rulemaking (see Section V.C of this preamble).

F. Affordability and Equity

In addition to considering environmental justice impacts, we have examined the effects of the standards on affordability of vehicles and transportation services for low-income households in Section VII.L of this preamble and Chapter 8.4 of the RIA. As with the effects of the standards on vehicle sales discussed in Section VII.B of this preamble, the effects of the standards on affordability and equity depend in part on two countervailing effects: The increase in the up-front costs of new vehicles subject to more stringent standards, and the decrease in operating costs from reduced fuel consumption over time. The increase in up-front new vehicle costs has the potential to increase the prices of used vehicles, to make credit more difficult to obtain, and to make the least expensive new vehicles less desirable compared to used vehicles. The reduction in operating costs over time has the potential to mitigate or reverse all these effects. Lower operating costs on their own increase mobility (see RIA Chapter 3.1 for a discussion of rebound driving).

While social equity involves issues beyond income and affordability, including race, ethnicity, gender, gender identification, and residential location, the potential effects of the standards on lower-income households are of great importance for social equity and reflect these contrasting forces. The overall effects on vehicle ownership, including for lower-income households, depend heavily on the role of fuel consumption in vehicle sales decisions, as discussed in Section VII.M of this preamble. At the same time, lower-income households own fewer vehicles per household and are more likely to buy used vehicles than new. In addition, for lower-income households, fuel expenditures are a larger portion of household income, so the fuel savings that will result from this rule may be more impactful to these consumers. Thus, the benefits of this rule may be stronger for lower-income households even (or especially) if they buy used vehicles: As vehicles meeting the standards enter the used vehicle market, they will retain the fuel economy/GHG-reduction benefits, and associated fuel savings, while facing a smaller portion of the upfront vehicle costs; see Section VII.J of this preamble. The reduction in operating costs may also increase access to transportation services, such as ride-hailing and ride-sharing, where the lower per-mile costs may play a larger role than up-front costs in pricing. As a result, lower-income consumers may be affected more from the reduction in operating costs than the increase in up-front costs.

The analysis for this final rule projects that EVs and PHEVs will gradually increase to about 17 percent market share by MY 2026, although the majority of vehicles produced in the time frame of the final standards will continue to be gasoline-fueled vehicles (see Section III.B.3 of this preamble). EPA has heard from some environmental justice groups and Tribes that limited access to electric vehicles and charging infrastructure for electric vehicles can be a barrier for purchasing EVs. A recent report from the National Renewable Energy Laboratory estimates that public and workplace charging is keeping up with projected needs, based on Level 2 and fast charging ports per plug-in EV. 27 Comments received on the proposed rule point out both the higher up-front costs of EVs as challenges for adoption and their lower operating and maintenance costs as incentives for adoption. As noted previously, the higher penetration of EVs in the current analysis as compared to that of the proposed rule is in part an outgrowth of updated estimates of battery costs, which reduce the projected costs of EVs as a compliance path and is consistent with expectations that cost parity with conventional vehicles is in the process of being attained in an increasing number of market segments. A number of auto manufacturers commented on the importance of consumer education, purchase incentives, and charging infrastructure development for promoting adoption of electric vehicles. Some NGOs commented that EV purchase incentives should focus on lower-income households, because they are more responsive to price incentives than higher-income households. EPA will continue to monitor and study affordability issues related to electric vehicles as their prevalence in the vehicle fleet increases.

27 Brown, A., A. Schayowitz, and E. Klotz (2021). “Electric Vehicle Infrastructure Trends from the Alternative Fueling Station Locator: First Quarter 2021.” National Renewable Energy Laboratory Technical Report NREL/TP-5400-80684, https://afdc.energy.gov/files/u/publication/electric_vehicle_charging_infrastructure_trends_first_quarter_2021.pdf, accessed 11/3/2021.

II. EPA Standards for MY 2023-2026 Light-Duty Vehicle GHGs

A. Model Year 2023-2026 GHG Standards for Light-Duty Vehicles, Light-Duty Trucks, and Medium-Duty Passenger Vehicles

As noted, the transportation sector is the largest U.S. source of GHG emissions, making up 29 percent of all emissions. 28 Within the transportation sector, light-duty vehicles are the largest contributor, 58 percent, to transportation GHG emissions in the U.S. 29 EPA has concluded that more stringent standards are appropriate in light of our assessment of the need to reduce GHG emissions, technological feasibility, costs, lead time, and other factors. The MY 2023 through MY 2026 program that EPA is finalizing in this action is based on our assessment of the near-term potential of technologies already available and present in much of the fleet. This program also will serve as an important transition to a longer-term program beyond MY 2026. The following section provides details on EPA's revised standards and related provisions.

28 Inventory of U.S. Greenhouse Gas Emissions and Sinks: 1990-2019 (EPA-430-R-21-005, published April 2021).

29 Ibid.

EPA is finalizing revised, more stringent standards to control the emissions of GHGs from MY 2023 and later light-duty vehicles. 30 Carbon dioxide (CO2 ) is the primary GHG resulting from the combustion of vehicular fuels. 31 The standards regulate CO2 on a grams per mile (g/mile) basis, which EPA defines by separate footprint curves that apply to vehicles in a manufacturer's car and truck fleets. 32 The final standards apply to passenger cars, light-duty trucks, and medium-duty passenger vehicles (MDPVs). 33 As an overall group, they are referred to in this preamble as light-duty vehicles or simply as vehicles. In this preamble, passenger cars may be referred to as “cars,” and light-duty trucks and MDPVs as “light trucks” or “trucks.” Based on compliance with the final revised standards, the industry-wide average emissions target for new light-duty vehicles is projected to be 161 g/mile of CO2 in MY 2026. 34 Except for a limited extension of credit carry-forward provisions for certain model years discussed in Section II.A.4 of this preamble, EPA is not changing existing averaging, banking, and trading program elements.

30 See Sections III and VI of this preamble for discussion of our technical assessment and basis of the final standards.

31 EPA's existing vehicle GHG program also includes emissions standards for methane (CH4) and nitrous oxide (N2O), and credits for hydrofluorocarbons (HFCs) reductions from air conditioning refrigerants.

32 Footprint curves are graphical representations of the algebraic formulae defining the emission standards in the regulatory text.

33 As with previous GHG emissions standards, EPA will continue to use the same vehicle category definitions as in the CAFE program. MDPVs are grouped with light trucks for fleet average compliance determinations.

34 The reference to CO2 here refers to CO2 equivalent reductions, as this level includes some reductions in emissions of greenhouse gases other than CO2 , from refrigerant leakage, as one part of the A/C related reductions.