...

(a) General. This section clarifies the limits of the defined terms “employee pension benefit plan” and “pension plan” for purposes of Title I of the Act and this chapter by identifying certain specific plans, funds and programs which do not constitute employee pension benefit plans for those purposes. To the extent that these plans, funds and programs constitute employee welfare benefit plans within the meaning of section 3(1) of the Act and §2510.3-1, they will be covered under Title I; however, they will not be subject to parts 2 and 3 of Title I of the Act.

(b) Severance pay plans.(1) For purposes of title I of the Act and this chapter, an arrangement shall not be deemed to constitute an employee pension benefit plan or pension plan solely by reason of the payment of severance benefits on account of the termination of an employee's service, provided that:

(b)(1)(i) Such payments are not contingent, directly or indirectly, upon the employee's retiring;

(b)(1)(ii) The total amount of such payments does not exceed the equivalent of twice the employee's annual compensation during the year immediately preceding the termination of his service; and

(b)(1)(iii) All such payments to any employee are completed,

(A) In the case of an employee whose service is terminated in connection with a limited program of terminations, within the later of 24 months after the termination of the employee's service, or 24 months after the employee reaches normal retirement age; and

(B) In the case of all other employees, within 24 months after the termination of the employee's service.

(b)(2) For purposes of this paragraph (b),

(b)(2)(i) “Annual compensation” means the total of all compensation, including wages, salary, and any other benefit of monetary value, whether paid in the form of cash or otherwise, which was paid as consideration for the employee's service during the year, or which would have been so paid at the employee's usual rate of compensation if the employee had worked a full year.

(b)(2)(ii) “Limited program of terminations” means a program of terminations:

(A) Which, when begun, was scheduled to be completed upon a date certain or upon the occurrence of one or more specifiedevents;

(B) Under which the number, percentage or class or classes of employees whose services are to be terminated is specified in advance; and

(C) Which is described in a written document which is available to the Secretary upon request, and which contains information sufficient to demonstrate that the conditions set forth in paragraphs (b)(2)(ii)(A) and (B) of this section have been met.

(c) Bonus program. For purposes of title I of the Act and this chapter, the terms “employee pension benefit plan” and “pension plan” shall not include payments made by an employer to some or all of its employees as bonuses for work performed, unless such payments are systematically deferred to the termination of covered employment or beyond, or so as to provide retirement income to employees.

(d) Individual Retirement Accounts.(1) For purposes of title I of the Act and this chapter, the terms “employee pension benefit plan” and “pension plan” shall not include an individual retirement account described in section 408(a) of the Code, an individual retirement annuity described in section 408(b) of the Internal Revenue Code of 1954 (hereinafter “the Code”) and an individual retirement bond described in section 409 of the Code, provided that—

(d)(1)(i) No contributions are made by the employer or employee association;

(d)(1)(ii) Participation is completely voluntary for employees or members;

(d)(1)(iii) The sole involvement of the employer or employee organization is without endorsement to permit the sponsor to publicize the program to employees or members, to collect contributions through payroll deductions or dues checkoffs and to remit them to the sponsor; and

(d)(1)(iv) The employer or employee organization receives no consideration in the form of cash or otherwise, other than reasonable compensation for services actually rendered in connection with payroll deductions or dues checkoffs.

(e) Gratuitous payments to pre-Act retirees. For purposes of title I of the Act and this chapter the terms “employee pension benefit plan” and “pension plan” shall not include voluntary, gratuitous payments by an employer to former employees who separated from the service of the employer if:

(e)(1) Payments are made out of the general assets of the employer,

(e)(2) Former employees separated from the service of the employer prior to September 2, 1974,

(e)(3) Payments made to such employees commenced prior to September 2, 1974, and

(e)(4) Each former employee receiving such payments is notified annually that the payments are gratuitous and do not constitute a pension plan.

(f) Tax sheltered annuities. For the purpose of title I of the Act and this chapter, a program for the purchase of an annuity contract or the establishment of a custodial account described in section 403(b) of the Internal Revenue Code of 1954 (the Code), pursuant to salary reduction agreements or agreements to forego an increase in salary, which meets the requirements of 26 CFR 1.403(b)–1(b)(3) shall not be “established or maintained by an employer” as that phrase is used in the definition of the terms “employee pension benefit plan” and “pension plan” if

(f)(1) Participation is completely voluntary for employees;

(f)(2) All rights under the annuity contract or custodial account are enforceable solely by the employee, by a beneficiary of such employee, or by any authorized representative of such employee or beneficiary;

(f)(3) The sole involvement of the employer, other than pursuant to paragraph (f)(2) of this section, is limited to any of the following:

(f)(3)(i) Permitting annuity contractors (which term shall include any agent or broker who offers annuity contracts or who makes available custodial accounts within the meaning of section 403(b)(7) of the Code) to publicize their products to employees,

(f)(3)(ii) Requesting information concerning proposed funding media, products or annuity contractors;

(f)(3)(iii) Summarizing or otherwise compiling the information provided with respect to the proposed funding media or products which are made available, or the annuity contractors whose services are provided, in order to facilitate review and analysis by the employees;

(f)(3)(iv) Collecting annuity or custodial account considerations as required by salary reduction agreements or by agreements to forego salary increases, remitting such considerations to annuity contractors and maintaining records of such considerations;

(f)(3)(v) Holding in the employer's name one or more group annuity contracts covering its employees;

(f)(3)(vi) Before February 7, 1978, to have limited the funding media or products available to employees, or the annuity contractors who could approach employees, to those which, in the judgment of the employer, afforded employees appropriate investment opportunities; or

(f)(3)(vii) After February 6, 1978, limiting the funding media or products available to employees, or the annuity contractors who may approach employees, to a number and selection which is designed to afford employees a reasonable choice in light of all relevant circumstances. Relevant circumstances may include, but would not necessarily be limited to, the following types of factors:

(A) The number of employees affected,

(B) The number of contractors who have indicated interest in approaching employees,

(C) The variety of available products,

(D) The terms of the available arrangements,

(E) The administrative burdens and costs to the employer, and

(F) The possible interference with employee performance resulting from direct solicitation by contractors; and

(f)(4) The employer receives no direct or indirect consideration or compensation in cash or otherwise other than reasonable compensation to cover expenses properly and actually incurred by such employer in the performance of the employer's duties pursuant to the salary reduction agreements or agreements to forego salary increases described in this paragraph (f) of this section.

(g) Supplemental payment plans— (1) General rule. Generally, an arrangement by which a payment is made by an employer to supplement retirement income is a pension plan. Supplemental payments made on or after September 26, 1980, shall be treated as being made under a welfare plan rather than a pension plan for purposes of title I of the Act if all of the following conditions are met:

(g)(1)(i) Payment is made for the purpose of supplementing the pension benefits of a participant or his or her beneficiary out of:

(g)(1)(i)(A) The general assets of the employer, or

(g)(1)(i)(B) A separate trust fund established and maintained solely for that purpose.

(g)(1)(ii) The amount payable under the supplemental payment plan to a participant or his or her beneficiary with respect to a month does not exceed the payee's supplemental payment factor (“SPF,” as defined in paragraph (g)(3)(i) of this section) for that month, provided however that unpaid monthly amounts may be cumulated and paid in subsequent months to the participant or his or her beneficiary.

(g)(1)(iii) The payment is not made before the last day of the month with respect to which it is computed.

(g)(2) Safe harbor for arrangements concerning pre-1977 retirees.(i) Notwithstanding paragraph (g)(1) of this section, effective January 1, 1975 an arrangement by which a payment is made by an employer to supplement the retirement income of a former employee who separated from the service of the employer prior to January 1, 1977 shall be deemed not to have been made under an employee benefit plan if all of the following conditions are met:

(g)(2)(i)(A) The employer is not obligated to make the payment or similar payments for more than twelve months at a time.

(g)(2)(i)(B) The payment is made out of the general assets of the employer.

(g)(2)(i)(C) The former employee is notified in writing at least once each year in which a payment is made that the payments are not part of an employee benefit plan subject to the protections of the Act.

(g)(2)(i)(D) The former employee is notified in writing at least once each year in which a payment is made of the extent of the employer's obligation, if any, to continue the payments.

(g)(2)(ii) A person who receives a payment on account of his or her relationship to a former employee who retired prior to January 1, 1977 is considered to be a former employee for purposes of this paragraph (g)(2).

(g)(3) Definitions and special rules. For purposes of this paragraph (g)—

(g)(3)(i) The term “supplemental payment factor” (SPF) is, for any particular month, the product of:

(g)(3)(i)(A) The individual's pension benefit amount (as defined in paragraph (g)(3)(ii) of this section), and

(g)(3)(i)(B) The cost of living increase (as defined in paragraph (g)(3)(v) of this section) for that month.

(A) The term “pension benefit amount” (PBA) means, with regard to a retiree, the amount of pension benefits payable, in the form of the annuity chosen by the retiree, for the first full month that he or she is in pay status under a pension plan (as defined in paragraph (g)(3)(iii) of this section) sponsored by his or her employer or under a multiemployer plan in which his or her employer participates. If the retiree has received a lump-sum distribution from the plan, the PBA for the retiree shall be determined as follows:

(1) If the plan provides an annuity option at the time of the distribution, the PBA shall be computed as if the distribution had been applied on that date to the purchase from the plan of a level straight annuity for the life of the participant if the participant was unmarried at the time of the distribution or a joint and survivor annuity if the participant was married at the time of distribution.

(2) If the plan does not provide an annuity option at the time of the distribution, the PBA shall be computed as if the distribution had been applied on that date to the purchase from an insurance company qualified to do business in a State of a commercially available level straight annuity for the life of the participant if the participant was then single, or a joint and survivor annuity if the participant was then married, based upon the assumption that the participant and beneficiary are standard mortality risks.

(B) If the retiree has received from the plan a series of distributions which do not constitute a lump-sum distribution or an annuity, the PBA for the retiree shall be determined with respect to each distribution according to paragraph (g)(3)(ii)(A) of this section, or in accordance with a reasonably equivalent method.

(C) The term PBA, with regard to the beneficiary of a plan participant, means:

(1) The amount of pension benefits, payable in the form of a survivor annuity to the beneficiary, for the first full month that he or she begins to receive the survivor annuity, reduced by:

(2) Any increases which have been incorporated as part of the survivor annuity under the plan since the participant entered pay status or, if the participant died before the commencement of pension benefits, since the participant's date of death.

(D) Where a plan participant has commenced to receive his or her pension benefits in the form of a straight-life annuity, or another form of an annuity that does not continue after the participant's death in the form of a survivor annuity, no beneficiary of the participant will have a PBA.

(g)(3)(iii) The term “pension plan” means, for purposes of this paragraph (g), a pension plan as defined in section 3(2) of the Act, but not including a plan described in section 4(b), 201(2), or 301(a)(3) of the Act. The term also does not include an arrangement meeting all the conditions of paragraph (g)(1) or (g)(2) of this section or of an arrangement described in §2510.3–2(e). In the case of a controlled group of corporations within the meaning of section 407(d)(5) of the Act, all pension plans sponsored by members of the group shall be considered to be one pension plan.

(g)(3)(iv) The term “employer” means, for purposes of paragraph (g) of this section, the former employer making the supplemental payment. In the case of a controlled group of corporations within the meaning of section 407(d)(7) of the Act, all members of the controlled group shall be considered to be one employer for purposes of this paragraph (g).

(g)(3)(v) The term “cost of living increase” (CLI) means, as to any month, a percentage equal to the following fraction:

a – b

b

where a= the CPIU for the month for which a payment is being computed, and b= the CPIU for the first full month the retiree was in pay status. Where the CLI is calculated for the beneficiary of a plan participant, “b” continues to be equal to the CPIU for the first full month the retiree was in pay status. If, however, the participant dies before the commencement of pension benefits, “b” is equal to the CPIU for the first full month the survivor is in pay status.

(g)(3)(vi) The term “CPIU” means the U.S. City Average All Items Consumer Price Index for all Urban Consumers, published by the U.S. Department of Labor, Bureau of Labor Statistics. Data concerning the CPIU for a particular period can be obtained from the U.S. Department of Labor, Bureau of Labor Statistics, Division of Consumer Prices and Price Indexes, Washington, DC 20212.

(g)(3)(vii) Where an employer does not pay to a retiree the full amount of the supplemental payments which would be permitted under paragraph (g)(1) of this section, any unpaid amounts may be cumulated and paid in subsequent months to either the retiree or the beneficiary of the retiree. The beneficiary need not be the recipient of a survivor annuity in order to be paid these cumulated supplemental payments.

(5) Examples. The following examples illustrate how this paragraph (g) works. As referred to in these examples, the CPIU's for July through November of 1980 are as follows:

July 1980: 247.8

August 1980: 249.4

September 1980: 251.7

October 1980: 253.9

November 1980: 256.2

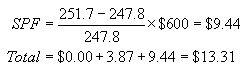

Example (1)(a). E is an employer. R received monthly benefits of $600 under a straight-life annuity under E's defined benefit pension plan after R retired from E and entered pay status on July 1, 1980. The amount that E may pay to R as supplemental payments under a welfare rather than pension plan with respect to the months of July through September of 1980 is computed as follows:

SPF for July 1980:

SPF for August 1980:

SPF for September 1980:

No supplemental payment may be made to R as a welfare plan payment with respect to July 1980, the month of retirement. The $3.87 that may be paid with respect to August 1980 may be paid at any time after August 31, 1980. The $9.44 that may be paid with respect to September 1980 may be paid at any time after September 30, 1980.

Example (1)(b). S is the beneficiary of R. Because R received pension benefits under a straight-life annuity, S will receive no survivor annuity from E after R's death. S thus will have no PBA after R's death and will not be eligible to receive any supplemental payments from E based on S's PBA. To the extent, however, that R did not receive supplemental payments from E to the maximum limit allowable under paragraph (g)(1), any amounts not paid to R may be cumulated and paid to S after R's death.

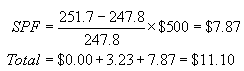

Example (2)(a). E is an employer. Q received monthly benefits of $500 in the form of a joint and survivor annuity under E's defined benefit pension plan since retirement from E on July 1, 1980. The amount that E may pay to Q as welfare rather than pension plan payments with respect to the months of July through September of 1980 is computed as follows:

SPF for July 1980:

SPF for August 1980:

SPF for September 1980:

No supplemental payment may be made as a welfare plan payment with respect to July 1980, the month of retirement. The $3.23 that may be paid with respect to August 1980 may be paid at any time after August 31, 1980. The $7.87 that may be paid with respect to September 1980 may be paid at any time after September 30, 1980.

Example (2)(b). Q dies on October 15, 1980 without having received any supplemental payments from E. T is the beneficiary of Q. E pays T a survivor's annuity of $300 beginning in November of 1980. The amount payable to T as a survivor annuity under the plan has not been increased since Q began to receive pension benefits. Thus, T's PBA is $300. The amount that E may pay to T as welfare rather than pension plan payments with respect to the months of July through November 1980 is computed as follows

SPF for July 1980=$0.00

SPF for August 1980=$3.23

SPF for September 1980=$7.87

SPF for October 1980:

(Note that T's “b” is equal to Q's “b”.)

SPF for November 1980:

Total that may be paid to T

The maximum E may pay T with respect to the months of July through November 1980 as welfare rather than pension plan payments is the sum of those months' SPFs, which is $33.58.

Example (3). Assume the same facts as in Example (1)(a), except that R elected to receive a lump-sum distribution rather than a straight-life annuity. If R is unmarried on July 1, 1980, R's PBA is $600 for the remainder of R's life. If R is married to S on July 1, 1980, the PBAs of R and S are based on the annuity that would have been paid under an election to receive a joint and survivor annuity. See paragraph (g)(3)(ii)(A)(1) of this section.

[40 FR 34530, Aug. 15, 1975, as amended at 44 FR 11763, Mar. 2, 1979; 44 FR 23527, Apr. 20, 1979; 47 FR 50240, Nov. 5, 1982; 47 FR 56847, Dec. 21, 1982; 81 FR 59476, Aug. 30, 2016; 81 FR 92653, Dec. 20, 2016; 82 FR 29237, June 28, 2017]